The following article is based on an interview with Transport, Highways and Mass Media Minister Dr. Bandula Gunawardena.

In 2022, the Government collected a total revenue of Rs. 1,751 billion from a combination of goods and services taxes (indirect taxes) imposed on all individuals, regardless of their income levels, and direct taxes levied directly on individuals. This substantial amount was contributed by a diverse range of professionals, including university professors, lecturers, doctors, engineers, and other academics.

It is imperative for any incoming Government to grapple with the formidable challenge of augmenting tax revenue, given the difficulty of placing additional tax burdens on the public. Out of the total income of Rs. 1751 billion, a substantial portion amounting to Rs. 1,265 billion has been allocated to cover Government employees’ salaries and pensions. In essence, 72 percent of the total tax revenue is channelled towards Government employees’ remuneration and pension disbursements.

It is imperative for any incoming Government to grapple with the formidable challenge of augmenting tax revenue, given the difficulty of placing additional tax burdens on the public. Out of the total income of Rs. 1751 billion, a substantial portion amounting to Rs. 1,265 billion has been allocated to cover Government employees’ salaries and pensions. In essence, 72 percent of the total tax revenue is channelled towards Government employees’ remuneration and pension disbursements.

It is rare for any Government to allocate more than three-quarters of its total tax revenue to civil servants and pension expenses. It raises a fundamental question as to whether any incoming government has viable alternative measures at its disposal to address the challenges posed by the significant salary and pension bill.

Secondly, from the total tax revenue of Rs. 1,751 billion, a significant portion amounting to Rs. 506 billion was allocated to subsidies, including programs such as Samurdhi assistance. This translates to approximately 28 percent of tax revenue being directed towards subsidies.

Numerical data demonstrates that the Government’s total tax revenue in 2022, which amounted to Rs. 1,751 billion, is insufficient to cover even two major expenses of that year. With Rs. 1,265 billion allocated for Government employees and pensions and an additional Rs. 506 billion for Samurdhi subsidies, the cumulative total of these two expenses reaches Rs. 1,771 billion.

Enduring challenge

Consequently, the government’s tax revenue falls short of covering these two primary expenses. This economic situation underscores the enduring challenge faced by successive Governments, where the primary account has historically been unable to generate a surplus.

These two expenses are just a part of the broader category of recurring expenses, which encompass the day-to-day operational costs of the Government and have a limited impact solely within the period in which the expenditure is accrued. Notably, one of Sri Lanka’s significant recurring expenses is the interest paid on the public debt, a substantial component of the overall expenditure.

In 2022, a staggering Rs. 1,565 billion was allocated for servicing the interest on both domestic and foreign debts. Despite the fact that there was no surplus left in the Treasury after disbursing salaries, pensions, and subsidies from the Rs. 1,751 billion of tax revenue, I have observed that the Opposition Leader and the Opposition MPs have not raised questions regarding how this substantial debt interest of Rs. 1,565 billion was covered.

In 2022, the expenditure earmarked for the development of infrastructure including roads, electricity, health, and education amounted to Rs. 715 billion. It raises the question of how this substantial capital expenditure of Rs. 715 billion was funded after allocating resources for salaries, pensions, and subsidies from the total tax revenue. In summary, based on the recorded figures, the government’s total tax and non-tax income amounts to Rs. 1,979 billion, falling short of the elusive Rs. 2,000 billion per year. The combined total of recurring and capital expenditure stands at Rs. 4,472 billion, resulting in a deficit of Rs. 2,493 billion between income and expenditure.

The Government has managed to bridge the deficit of Rs. 2,493 billion, despite incurring an expenditure of Rs. 4,472 billion while earning an income of less than Rs. 2,000 billion, through a combination of borrowing and printing of currency.

Incoming Governments are set to face a significant challenge, as they will need to engage in substantial borrowing to address the Budget Deficit. This challenge is compounded by the fact that the stock of blocked foreign debt due on 31 December 2022, stands at US$ 36 billion. As part of the debt restructuring program, incoming governments will be responsible for repaying 37 percent of this debt stock over the next 5-6 years.

A significant portion of the outstanding foreign debt, approximately 51 percent, is set to mature over the next 6-20 years, with an additional 12 percent of the debt stock requiring repayment even beyond the 20-year mark. Consequently, regardless of which Government assumes power in Sri Lanka, economic planning for the country must be structured to accommodate the repayment of these foreign debts until at least the 100th anniversary of Independence in 2048.

Any political party or coalition aspiring to govern will face formidable challenges in governance until this foreign debt is effectively restructured. The ability to address these issues with concrete numerical data will be critical for their governance success. It is important to note that Sri Lanka’s agreement with the International Monetary Fund (IMF) includes provisions for seeking loans from the international market at potentially high interest rates by 2027.

Any political party or coalition aspiring to govern will face formidable challenges in governance until this foreign debt is effectively restructured. The ability to address these issues with concrete numerical data will be critical for their governance success. It is important to note that Sri Lanka’s agreement with the International Monetary Fund (IMF) includes provisions for seeking loans from the international market at potentially high interest rates by 2027.

If the conditions outlined in the financial fund’s program are meticulously met by 2027, there is potential for the country’s foreign reserves to reach US$ 14 billion. In conjunction with the anticipated macroeconomic adjustments, there is also the possibility of issuing a development bond worth US$ 1,500 billion in the international market.

The challenge becomes more evident when considering that the value of sovereign bonds maturing up to 2029, obtained after the Good Governance government came to power in 2015, exceeds US$ 12 billion. In stark contrast, Sri Lanka’s total gross foreign assets currently stand at US$ 3.8 billion. To put this into perspective, a relatively small City State like Singapore boasts gross foreign assets totalling a staggering US$ 763 billion, underscoring the significant disparity.

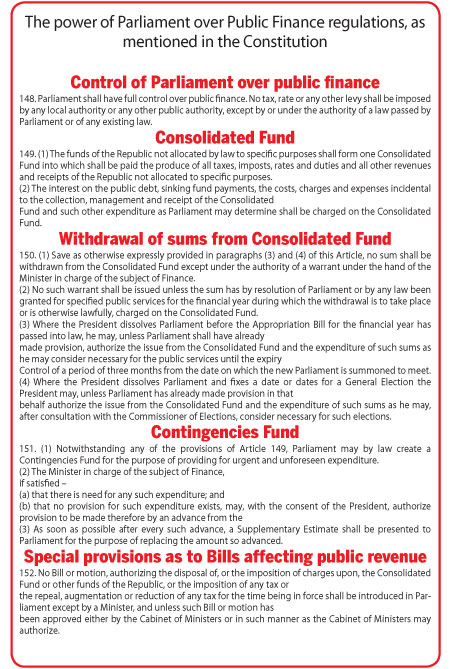

Parliament bears a tremendous responsibility for managing public finances and addressing the substantial international and national financial and exchange crisis highlighted herein. Debating these critical issues for extended periods is not only necessary but also essential to charting a path forward and formulating sound financial policies that can mitigate the challenges.

In Parliamentary traditions worldwide, debates often revolve around crucial financial aspects such as Government income, expenditure, budget, deficits, debt, foreign investment, taxes, and various revenue sources. Engaging in these enlightening discussions is vital for effective governance. It is regrettable that in Sri Lanka, such discussions may not always receive the attention and importance they deserve. After all, Parliament is responsible for Finances.

The parliamentary debates that receive extensive media coverage often involve swearing or humour, detracting from more substantive discussions on important financial matters. It is crucial for the informed citizens of this country to guide me on whether I should focus on providing comedic content or address the critical issue of public financial management in my role as the Minister of Mass Media. Elected MPs should prioritise responsible governance to prevent the country from facing financial insolvency.

Responsibility

The responsibility for these issues primarily falls on former Presidents and the Parliament of this country. Two key factors have contributed to the country’s financial distress: A massive public budget deficit that is unsustainable in the long term; A persistent long-term deficit in the current account of the international Balance of Payments.

Political parties lack political solutions for these two challenges, and the solutions lie primarily in the economic domain. To address these issues, it is imperative for political parties to exhibit responsible leadership and engage in constructive and cooperative dialogues with international bodies such as the IMF, the World Bank, the Asian Development Bank (ADB) and various nations. This approach is vital to rescue the country from the severe economic challenges it currently faces.

During President Ranil Wickremesinghe’s tenure as Prime Minister, the Financial Management Act No. 3 of 2003 was passed in Parliament amidst much debate while I served as the Minister of Finance. This act involved numerous discussions and led to the formulation of three key regulations under a single legislative measure.

Starting from 2006, the Government aimed to limit the budget deficit to 5 percent of the Gross Domestic Product (GDP), with a maximum allowable budget deficit of 15 prcent, regardless of the governing party.

The Act called for a reduction in the total outstanding foreign public debt as a percentage of GDP to 60 percent by 2016, and subsequent Governments were expected to maintain this threshold. The Government was mandated to allocate 4.5 percent of the Gross Domestic Product (GDP) for servicing public debt. Adhering to these fiscal regulations and maintaining financial discipline would have likely contributed to better economic stability and prevented the country from experiencing financial distress.

Dr. P. B. Jayasundera, who served as the Secretary of the Ministry of Finance and was a member of the Monetary Board during the administrations that was appointed after our Government was ousted and subsequent leaders, who held Jayasundera’s speeches in high regard, made frequent changes to Parliamentary laws, leading to manipulations in State financial management and international balance of payments that ultimately drove the country to bankruptcy.

Dr. P. B. Jayasundera, who served as the Secretary of the Ministry of Finance and was a member of the Monetary Board during the administrations that was appointed after our Government was ousted and subsequent leaders, who held Jayasundera’s speeches in high regard, made frequent changes to Parliamentary laws, leading to manipulations in State financial management and international balance of payments that ultimately drove the country to bankruptcy.

The following excerpt is from my inaugural speech delivered 34 years ago, on 20 March 1989, during my first address to Parliament: “In 1977, Sri Lanka’s foreign debt stood at Rs. 13,321 million.

Presently, our foreign debt has surged to Rs. 161,914 million. Over this period, the increment in foreign loans signifies a staggering 1,115 percent increase. This means that every individual in our country now carries a debt burden abroad, amounting to Rs. 10,100 rupees each.

As a consequence of this mounting debt burden, we find ourselves obligated to allocate a significant portion of our foreign exchange earnings to service this debt. Presently, we are expanding 28.8 percent of our foreign exchange income, generated by exporting goods and services, on interest payments and loan instalments to other nations. When a country dedicates 30 percent of its income derived from exporting its products and services to pay interest to foreign entities and settle loan obligations, it leaves only 70 percent of that income to address pressing national needs.

With the continuous depreciation of the Rupee and the accumulation of more loans, our economy is now grappling with a debt burden that is becoming increasingly unsustainable.

The economic situation is reaching a critical point where it can no longer withstand the weight of this debt burden. It is apparent that the economy has already crossed the threshold into an unsustainable level of debt, with severe consequences.

Under the policies implemented by your Government, the unemployment-employment crisis in our country has intensified. A staggering one million young individuals in our nation lack job security. Currently, over 20 percent of working-age individuals who are willing and able to contribute to the workforce find themselves without employment.

If you were to survey a hundred young individuals and inquire about their activities, the resounding response you would receive is, “There is nothing to do”. This sentiment is echoed by countless young men and women in our country. It is imperative that we recognize the gravity of this issue and take decisive action to address it.

Our nation is grappling with a significant youth unemployment crisis, with approximately 40 percent of individuals under the age of 25 lacking employment opportunities.

Moreover, we are witnessing educated individuals also facing unemployment challenges, with around 35 percent of those who have successfully completed their general and advanced levels struggling to secure jobs.

When educated youth find themselves without employment, they often feel powerless and have limited recourse or support. This predicament often leads them to express frustration with the social system in which they were born. (Parliamentary Hansard Column No. 20 of March 20, 1989, Pages No. 733 and 734).

Buddha’s teachings

I would like to share a verse from the Dhammapada, the Buddha’s teachings, which provides solace. This verse is my response to those who may label my discussions on State revenue and expenditure as nonsense, as depicted in a recent cartoon in a Sinhala newspaper. Appassutayan puriso. Balivaddova jirati mansani tassa vaddhanti. Panna tassa na vaddhati. The less educated age much like an ageing ox. They gain in physical stature but not in mental acuity.

Compiled by Cyril Liyanaarachchi and translated by Maneshka Borham.